King County Buyer Rebate: How Much Can You Save?

Flat Fee Nic Chambers February 14, 2026

Flat Fee Nic Chambers February 14, 2026

The median home price in King County is hovering around $850,000. That means a traditional buyer’s agent commission usually 2.5% is about $21,250.

Most buyers never see that money. It just… disappears into the transaction.

But a big chunk of that commission doesn’t have to go to the agent. In Washington, it can come back to you as a buyer's rebate. So instead of stressing about closing costs, rate buydowns, or how much cash you’ll have left after escrow, you could be walking away with $15,000–$45,000 back in your pocket, depending on the price point.

And yes, it’s completely legal in King County. It’s just not something most agents love to advertise.

Nic Chambers’ flat-fee buyer model flips the usual math. Instead of paying a percentage that scales up with the home price (even though the work doesn’t), you pay a clear, upfront fee. The rest of the buyer-side commission? Rebated back to you.

Honestly, once you see the numbers, it’s hard to unsee them. If you want a quick estimate for your price range, you can use the rebate calculator. But first, let’s slow down and let’s show you how this actually works in King County.

A buyer rebate is simple in theory, but confusing in practice, mostly because no one explains it cleanly. Here’s what’s really happening behind the scenes.

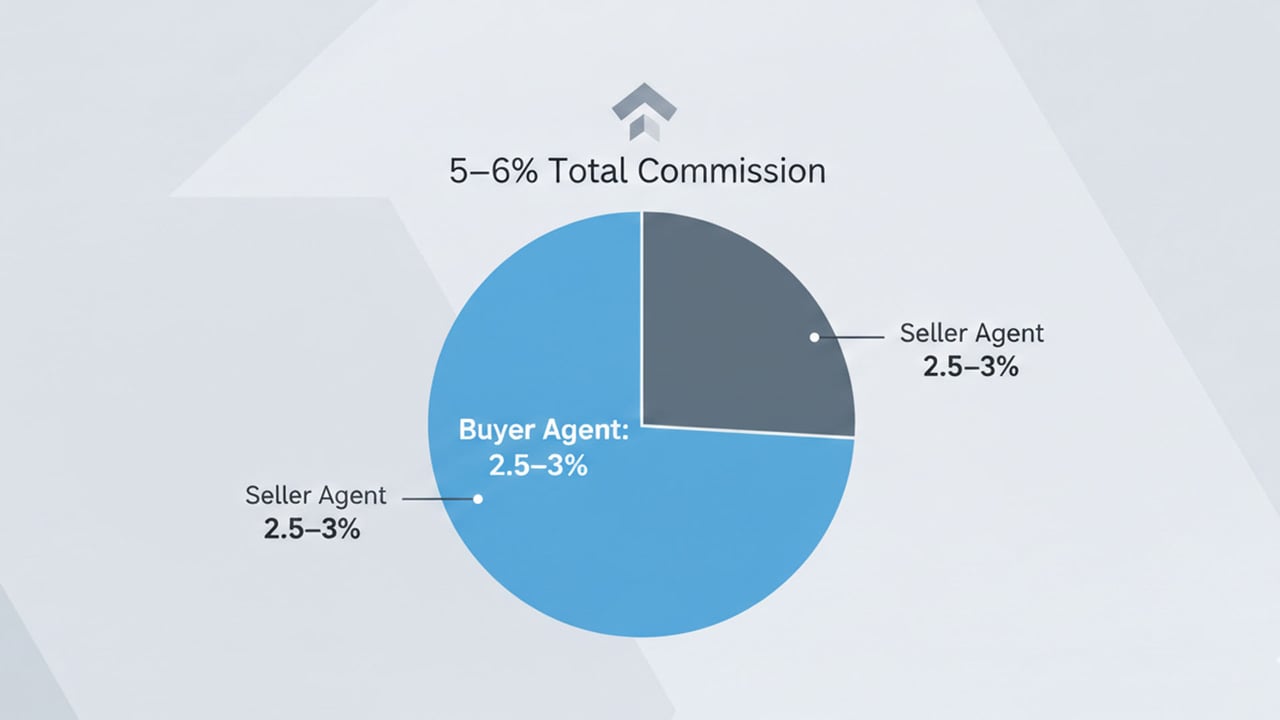

Traditionally, sellers agree to pay a total commission of 5–6%, which gets split between the listing agent and the buyer’s agent. In King County, the buyer’s side is usually 2.5–3%.

That structure existed for decades. Buyers rarely questioned it because they were told, “You’re not paying your agent…the seller is.”

But after the 2024 NAR settlement, that language matters a lot more. Buyers now sign buyer-broker agreements that spell out how much their agent gets paid and how. That fee is negotiable. Always has been, but now it’s explicit.

A buyer rebate happens when your agent earns that commission and then returns a portion of it to you at closing. Same transaction. Same MLS. Same escrow process. Different economics.

Flat-fee model (Chambers NW): You pay a fixed fee for representation. Let’s say, for example, it’s around $13,000. If the buyer-broker commission on your home is $28,000, the remaining $15,000 comes back to you as a rebate.

The home price goes up? Your rebate goes up. The work stays the same.

Percentage-based rebate models:

Some agents rebate 1–2% of the purchase price. That can look attractive, but it often comes with caps, exclusions, or reduced service, and it still ties cost to price.

At lower price points, the difference is small. At $1.2M, $1.8M, $3M+, the flat-fee model almost always wins. This is why high-priced King County buyers quietly use rebates while everyone else assumes it’s “not a thing.”

Yes. Completely.

Washington state allows commission rebates. Unlike Oregon or Alaska, there’s no prohibition. Escrow companies here handle them all the time.

From a tax standpoint, the IRS treats a buyer rebate as a reduction in purchase price, not income. That means it lowers your cost basis instead of creating a tax bill. (Always confirm with your CPA)

And from an escrow perspective? It shows up right on the closing statement. No side checks. No weird timing. Just a few dollars are required from you to close.

Which is why rebates are most powerful when rates are high, and cash is tight.

Because “buyer rebate” sounds abstract until you tie it to an actual street, an actual price, and an actual closing statement. So let’s do that.

Seattle prices move fast, but the math is surprisingly consistent.

Take a $1.2M home on Capitol Hill. A typical buyer-broker commission at 2.5% is $30,000.

With a flat-fee model, after the agent fee, you’re often looking at $17,000 coming back to you at closing. Ballard. Fremont. Queen Anne. Same story.

That rebate alone can:

Cover most or all closing costs (usually $8K–$15K)

Pay for furniture without touching savings

Or buy down your interest rate and quietly save tens of thousands over time

And because Seattle's offers are competitive, the rebate stays in the background. You’re not weakening your offer. You’re just fixing your math after it’s accepted.

This is where flat-fee rebates really stretch their legs. Bellevue’s median price is around $1.3M. At 2.5%, that’s $32,500 in buyer-side commission.

Subtract a flat fee, and you’re often rebating roughly $19,500. Redmond, Kirkland, Issaquah, similar ranges, similar outcomes. Eastside buyers tend to use rebates strategically:

Mortgage rate buydowns

Small remodels before move-in

Padding post-close cash so the purchase doesn’t feel like financial whiplash

Renton. Kent. Auburn. Federal Way. Let’s say you buy at $750,000. Buyer-side commission at 2.5% = $18,750. After a flat fee, your rebate can land about $5,750.That might not sound dramatic compared to luxury numbers, but in this price range, it’s impactful:

Property taxes for a year

HOA dues without stress

An emergency fund that doesn’t get wiped out by the move

For first-time and move-up buyers, this is often the difference between “tight” and “comfortable.”

This is where traditional commission models quietly stop making sense. A $3M home means $75,000 on the buyer side at 2.5%. Even after a full-service flat fee, buyers can see $62,000 rebate.

In Medina, Mercer Island, and Clyde Hill, this money often goes toward:

Landscaping and exterior work

Interior upgrades before move-in

Offsetting capital gains from a previous sale

Same contracts. Same negotiation. Same protections. Just… a very different financial outcome.

Now for the part people worry about. “What if a rebate messes up my offer?” It doesn’t, if you use it correctly.

In competitive markets, you don’t advertise the rebate in your offer. You keep your price clean and strong. The rebate shows up at closing instead:

Lower cash-to-close

Credits toward closing costs

Or a lender-approved rate buydown

In slower or balanced markets, you might combine a price reduction with a rebate. But honestly, most King County buyers benefit more from keeping the offer clean and handling savings after acceptance.

Lenders do have rules. Rebates can never be used for down payments, but they’re usually fine for closing costs and rate buydowns. This gets coordinated early, so there are no surprises.

There’s a myth that rebate buyers are “less serious.” That only applies when the rebate changes the offer structure. A flat-fee model doesn’t.

Your offer price is your offer price. Your earnest money is your earnest money. Your terms stand on their own. The rebate simply gives you flexibility:

You can stomach inspections more confidently

You can fund small repairs without renegotiation

You can buy down your rate and potentially reduce long-term interest costs.

This isn’t a stripped-down service. You still get:

Full MLS access and market analysis

Showing coordination and offering a strategy

Negotiation, inspection guidance, and contract expertise

Transaction management through close

The only real difference? You don’t overpay just because the home costs more.

If you want to see what this looks like for your specific price range, the rebate calculator will give you a clean estimate. And if you want to talk through strategy, especially in a competitive neighborhood, a discovery call is usually the fastest way to get clarity.

You know the ones. Ten offers. Escalation clauses flying. Sellers are laser-focused on certainty.

In these situations, the priority is clean terms, speed, and confidence. A buyer rebate does not harm your offer. It simply stays in the background and is applied at closing. If winning requires:

Waiving contingencies

Compressing timelines

Strengthening non-price terms

Those decisions stand on their own. The rebate doesn’t interfere with execution; it just improves the buyer’s financial outcome after acceptance. In ultra-competitive markets, the rebate simply ensures the numbers make more sense once the deal is secured.

Rebates aren’t always the right move. And anyone who says otherwise hasn’t actually negotiated deals here. Here are the conditions when it’s not the right move…

On smaller purchases, the savings gap between traditional commission and flat fee narrows. In those cases, the question becomes less about maximizing dollars and more about fit, service, and comfort level. And that’s okay.

Some buyers want hand-holding, where you would want Nic to be by your side every step of the way. Flat-fee models at Chambersnw tend to attract buyers who value:

Clear thinking

Direct communication

Strong negotiation over cheerleading

Rebates are a tool; when used intentionally, they’re powerful. When forced, they’re not.

The post–NAR settlement world isn’t temporary. It’s a permanent shift. Buyers are now explicitly agreeing on how their agent gets paid. That makes compensation visible. Negotiable. Comparable.

Which means buyers are going to start asking harder questions: “Why am I paying more just because the house costs more?” “What am I actually getting for that fee?” “Where does this money go if I don’t use a traditional model?”

Buyer rebates answer those questions directly. They align cost with value. They remove percentage-based bloat. And they give buyers leverage in a market where rates and prices already demand discipline.

Every year, many King County buyers leave significant money on the table simply because no one shows them another option. Same homes. Same contracts. Same protections. Just better economics.

Flat-fee buyer representation doesn’t change how you buy. It changes how much of your own money you get to keep.

If you’re even loosely considering a purchase, now or later this year, the smartest next step is to run the numbers for your price range.

Use the rebate calculator to see what you’d actually save, or schedule a consultation with a buyer rebate agent in King County if you want to talk strategy for your neighborhood.

Nic works across Bellevue, Bothell, Issaquah, and Seattle and knows where rebates help, where they don’t, and how to use them without weakening your position. And honestly?

Once you see the numbers, you’ll never look at buyer commissions the same way again.

Stay up to date on the latest real estate trends.

Flat Fee

Right agent for selling your Issaquah Home

A local real estate guide to navigating Issaquah’s unique neighborhoods, micro-markets, and buyer dynamics with clarity and confidence.

Flat Fee

A Complete Guide to Accurate Home Valuation, Buyer Behavior, and Maximizing Your Net Proceeds

Understanding Why Homebuyers Ultimately Fund Buyer-Agent Commissions, and How a Flat-Fee Model Can Save You Thousands.”

Contact Details

Nic Chambers

12520 TOTEM LAKE BLVD NE STE 271 KIRKLAND WA 98034