Capital Gains Tax When Selling a Home in King County: What Kirkland & Bellevue Sellers Need to Know

selling and buying Nic Chambers June 29, 2026

selling and buying Nic Chambers June 29, 2026

Most Eastside homeowners who sell their primary residence won't owe capital gains tax at all. But the rules that determine whether you're in the clear or not are worth understanding before you list. Because the ones who get surprised at closing are almost always the ones who assumed they were fine without checking.

After more than 200 Eastside transactions, I've found that taxes are one of the most misunderstood parts of the selling process. Many homeowners assume they'll owe far more than they actually will, while others don't realize they may have taxable gains until they're already preparing to close.

This guide walks through what capital gains tax actually means for home sellers in King County, how Washington state fits into the picture (it's less scary than you've heard), when the federal exclusion protects you, and when it doesn't.

Washington state enacted a capital gains excise tax in 2022, and in 2025, SB 5813 added a second tier, bringing rates to 7% on gains between $278,000 and $1 million, and 9.9% on gains above $1 million. If you've seen those headlines, it's easy to panic.

Real estate is explicitly exempt. Every category of real property, primary residence, investment property, and commercial real estate, is excluded from Washington's capital gains excise tax by statute. That exemption survived the 2025 rate increase and remains intact as of 2026.

So if someone in your life told you Washington is now taxing home sales at 9.9%, they're not quite right. The tax exists. It just doesn't apply to your home.

No state income tax means no state-level tax on the gain from your home sale, period. The only Washington tax that applies when you sell real estate is REET, the Real Estate Excise Tax, which is a transaction tax based on your sale price, not your profit. We covered REET in detail in our seller cost guide, but the short version: it's graduated, ranges from 1.1% to 1.28% on most Eastside sales, and you can't negotiate it.

For most homeowners, capital gains considerations are primarily a federal issue.

The $250,000 / $500,000 Exclusion: How It Works

Section 121 of the tax code is the rule that protects most homeowners from federal capital gains tax on a home sale. If you've owned your home and lived in it as your primary residence for at least 2 of the last 5 years before selling, you can exclude a substantial portion of your gain from federal taxes.

Many homeowners who qualify for the exclusion ultimately owe no federal capital gains tax.

Bellevue's median home price is currently around $1.48 million. Kirkland's NE King County median sits near $1.3 million. This comes up most often with long-time homeowners in neighborhoods such as Bridle Trails, West Bellevue, Houghton, and Finn Hill, where appreciation over the last decade has been substantial enough that gains can exceed federal exclusion thresholds. A lot of long-term Eastside homeowners have built gains well above $500,000, which means some portion of their profit could be taxable at the federal level even after the exclusion applies.

This isn't a reason to panic. It's a reason to know your numbers before you sell — not after.

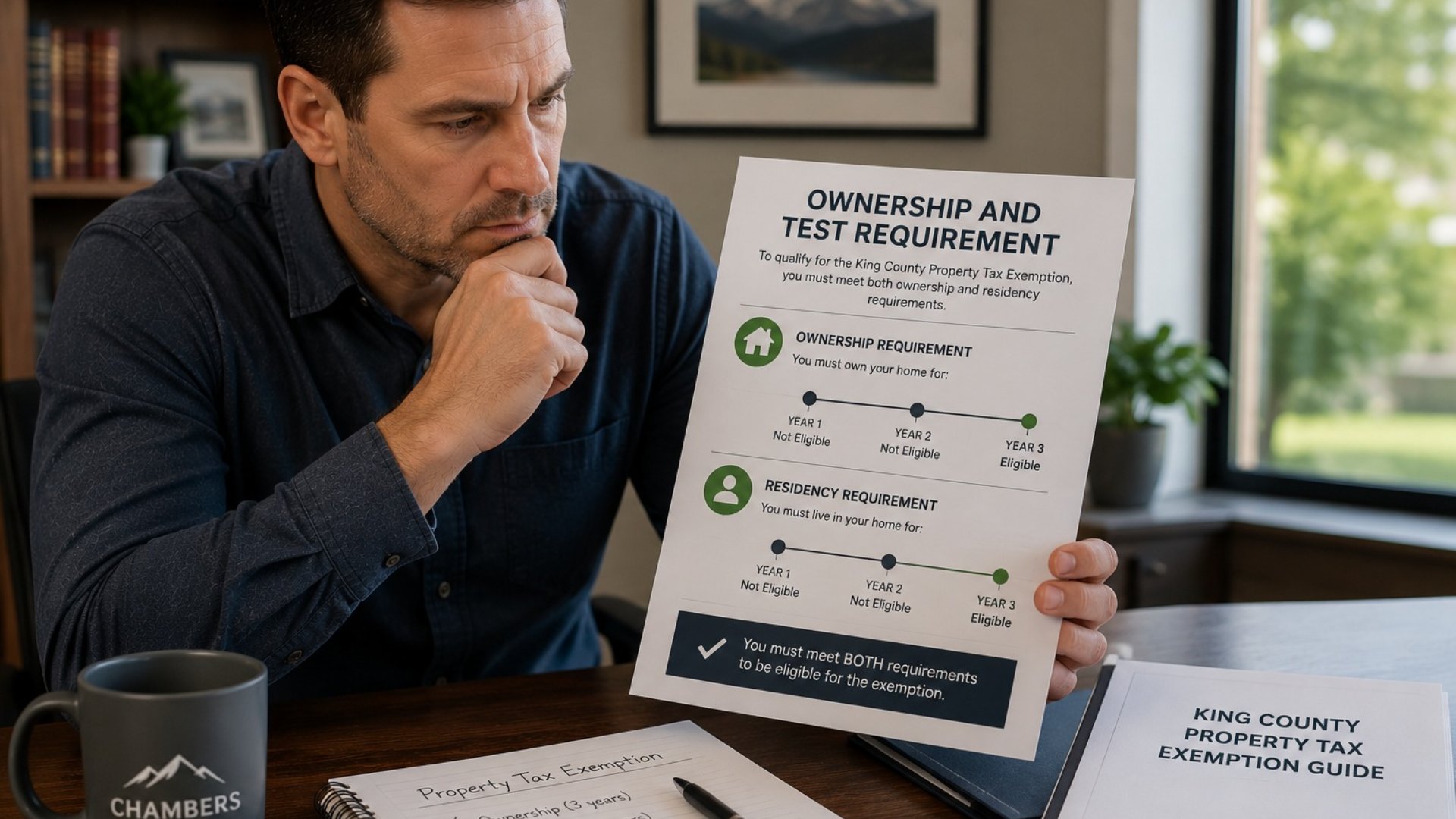

To qualify for the full Section 121 exclusion, you need to meet two tests:

Ownership test: You must have owned the home for at least 2 years within the last 5 years.

Use test: You must have lived in it as your primary residence for at least 2 years within the same 5-year window. The two years don't have to be consecutive.

One more rule: you can only use this exclusion once every two years. So if you sold another home and claimed the exclusion recently, you may need to wait.

Life doesn't always follow a clean two-year schedule. If you're selling early due to a job relocation, health issue, or other unforeseen hardship, you may still qualify for a partial exclusion proportional to how long you lived there. The IRS defines 'unforeseen circumstances' fairly broadly; it's worth asking a tax advisor if your situation is messy.

Let's say you bought a Kirkland home in 2010 for $500,000 and you're selling today for $1.5 million. Your gain is $1 million. If you're married filing jointly, the $500,000 exclusion wipes out half of that, but the remaining $500,000 is potentially taxable.

The federal long-term capital gains rate depends on your overall taxable income for 2026:

Most Eastside sellers in the $500k–$1M gain range will land in the 15% bracket after the exclusion, unless your household income is already high. That's NOT nothing, but it's also not a crisis if you've planned for it.

If your modified adjusted gross income (MAGI) exceeds $200,000 for single filers or $250,000 for married couples, the Net Investment Income Tax kicks in at 3.8% on capital gains. This applies to taxable gains above the Section 121 exclusion.

For high-earning tech households on the Eastside, which is a lot of Kirkland and Bellevue, this is often the tax that shows up unexpectedly. It stacks on top of the 15% or 20% long-term rate. Combined, a high earner with $300,000 in taxable gain after the exclusion could be looking at 18.8% to 23.8% federal tax on that portion.

Again: not a reason to avoid selling. But definitely a reason to run the actual numbers before closing.

Selling a home you've owned for less than 2 years or lived in for less than 2 of the last 5 years means the Section 121 exclusion doesn't apply. Your gain is subject to federal capital gains tax in full.

If you've been in your Bellevue home for 18 months and need to sell due to a job change or life event, don't assume you're stuck. Ask a tax advisor about the partial exclusion rules first; you may still be able to exclude a proportional amount.

If the home you're selling was a rental at any point, the tax picture gets more complicated. You may face depreciation recapture taxed at up to 25% on the portion that was previously depreciated. The Section 121 exclusion still applies to periods when the home was your primary residence, but it doesn't apply to periods of non-qualifying use.

This is a situation where talking to a CPA before you list isn't optional; it's how you avoid a painful surprise at tax time.

If you're not sure whether the exclusion fully covers your situation, the first step is understanding your estimated gain, selling costs, and likely net proceeds before putting your home on the market.

Your 'gain' isn't just the sale price minus the purchase price. It's sale price minus your adjusted cost basis, and your basis increases with every capital improvement you've made to the home.

Kitchen remodel, new roof, added square footage, major landscaping, HVAC replacement, all of these can add to your basis if you've kept records. On a home where you've spent $80,000 in improvements over 10 years, that's $80,000 less in taxable gain. On a $1.5M sale, that matters.

What counts: Permanent improvements that add value or extend the life of the home. What doesn't count: routine repairs and maintenance.

If you haven't been tracking these, dig up old receipts, contractor invoices, and permit records. Even a partial recovery is worth it.

Your real estate commission, escrow fees, transfer taxes, and other closing costs are deductible from your gain. So if you sell for $1.4M but pay $70,000 in combined selling costs, your actual realized gain is calculated on $1.33M, not $1.4M.

This is another reason a detailed net sheet matters before you finalize your plans. See what you actually net, after taxes, after costs, after everything.

If you're close to a tax bracket threshold, timing your sale to straddle two tax years can sometimes reduce your effective rate. This is more nuanced than it sounds and depends entirely on your overall income picture for both years. Worth a conversation with a CPA if you're close to the 15%/20% threshold.

For most Eastside homeowners selling their primary residence, capital gains tax isn't the issue it's feared to be. Washington doesn't tax your home sale. The federal exclusion protects up to $500,000 in gain for married couples. And if your gain is below that threshold, you may owe nothing at all.

I've had conversations with Eastside homeowners who assumed they would owe hundreds of thousands in taxes because their home had appreciated significantly. In many cases, once the Section 121 exclusion and adjusted cost basis were properly accounted for, their tax exposure was far lower than expected.

But 'most' isn't 'all.' Long-term Eastside homeowners with significant appreciation, high household incomes, or homes with rental histories are the ones who need to do their homework before listing. The rules are manageable; they just require knowing where you stand.

The best time to figure this out is before your home hits the market, not after you've accepted an offer. Run your numbers, talk to a tax advisor if your situation is complicated, and go into your sale with a clear picture of what you'll actually walk away with.

That's the whole point, knowing your real net, not just your sale price. Estimate Your Net After Taxes OR Book a Free Seller Consultation with Chambers NW.

Stay up to date on the latest real estate trends.

selling and buying

selling and buying

selling and buying

selling and buying

Contact Details

Nic Chambers

11901 NE Village Plaza, Suite 271 Kirkland WA 98034